Federal Budget 2026–27: what changed (and what didn't) for your fitness business

Federal Budget 2026–27

What it means for Australian gym, studio and wellness operators.

__

Executive summary

The 2026/27 Federal Budget has a handful of measures that will actually matter for fitness and wellness operators. For most operators, the biggest opportunities sit around cash flow, equipment investment, and a bit more breathing room for businesses going through heavy growth phases.

While not every measure will apply to every business model, the broader direction is clear: operators investing in growth, technology and long-term operational efficiency are being given more room to move than they were before.

This whitepaper breaks down the Budget measures most relevant to the fitness and wellness industry, what they mean in practice, and where operators may want to review strategy alongside their accountant or adviser.

SNAPSHOT OF THE CHANGES

The five things that matter most

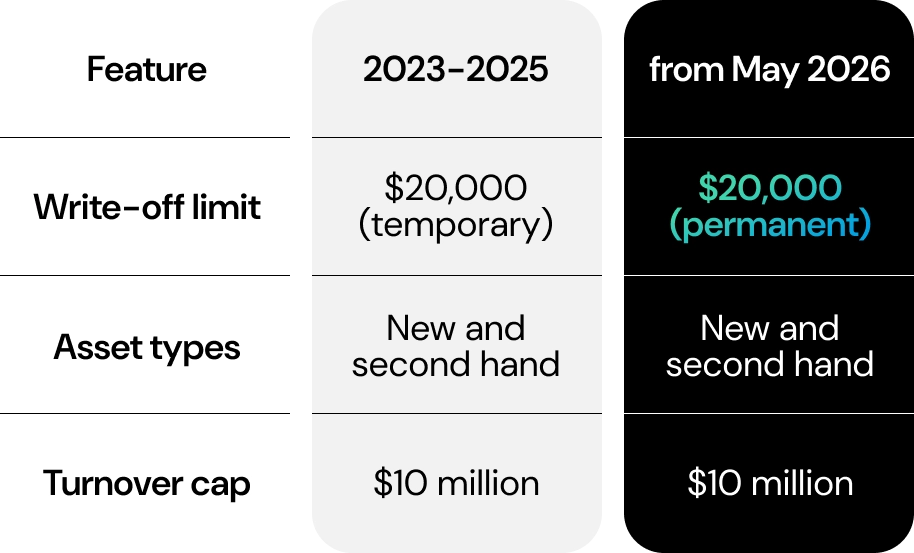

Permanent $20,000 instant asset write-off from 1 July 2026

Big one for operators investing in equipment, recovery spaces, fit-outs and in-club tech. No more annual uncertainty waiting on extensions.

Two-year loss carry-back for companies with turnover up to $1 billion

Businesses reinvesting heavily into expansion or new locations may be able to pull back tax paid in earlier profitable years.

Loss refundability for start-up studios from 1 July 2028

New studios in their first two years of operation may be eligible for cash refunds tied to PAYG withholding and FBT already paid on employee wages.

$1,000 instant work-related deduction from 2026–27

A simplified deduction for individual taxpayers, including employed trainers, instructors and fitness staff doing their own return.

PAYG instalment flexibility from 1 July 2027

New monthly payment options and dynamic installment calculations aim to better align tax payments with real-time business performance.

Setting the scene

Running a fitness or wellness business in Australia has gotten meaningfully more expensive over the past few years. Equipment cycles are faster, boutique and recovery concepts keep pushing fit-out costs up, and member expectations around technology just keep rising. On top of that, wages, rent and energy costs have all been heading in the same direction.

Against that backdrop, the 2026/27 Federal Budget brings in several measures aimed at supporting businesses investing in growth, infrastructure and long-term capability.

Plenty of the headline stuff isn’t brand new. Both the instant asset write-off and loss carry-back provisions came out of COVID-era support packages. What’s changed is that they’re now permanent and more widely accessible. Operators can actually plan equipment upgrades and expansion without waiting on annual Budget extensions or second-guessing whether a policy will still be around come July.

For incorporated studios and multi-site operators, the return of loss carry-back also gives more flexibility during heavy investment periods, particularly when scaling into new locations or doing major facility upgrades.

It’s worth noting a few things that were speculated ahead of the Budget and didn’t happen: cuts to small business CGT concessions and changes to trust taxation weren’t introduced. Changes to capital gains tax and negative gearing were announced, but those apply to property investments acquired after 1 July 2027 and sit well outside the day-to-day operating structure of most gyms and studios.

1. Permanent $20,000 instant asset write-off

EFFECTIVE 1 JULY 2026 | SMALL BUSINESSES WITH TURNOVER UNDER $10M

WHAT IT IS

Eligible small businesses can immediately write off the full cost of business assets under $20,000, rather than depreciating them over several years. The threshold applies per asset, so multiple purchases under $20,000 can each be written off in the same financial year.

The write-off has existed in various temporary forms before, but the shift here is permanence. From 1 July 2026, there’s no need to wait on annual extensions or rush purchasing decisions because of EOFY uncertainty.

WHY IT MATTERS FOR FITNESS AND WELLNESS OPERATORS

For a lot of gyms, studios and wellness businesses, a large chunk of operational equipment sits comfortably under the $20,000 threshold. That includes:

- Strength and cardio equipment

- Reformer Pilates beds, spin bikes and rowing machines

- Recovery infrastructure like ice baths, compression systems and smaller saunas

- AV systems, class screens and in-club technology

- Body composition scanners and performance tracking equipment

- Reception fit-outs, tablets and business devices

The flexibility is the real value here. Investment decisions can be made around what the business actually needs, not around temporary tax deadlines or EOFY speculation.

This matters most for operators modernising member experience through technology, recovery offerings and premium in-club infrastructure, where ongoing reinvestment has become part of staying competitive. Equipment upgrades, recovery expansions and technology investments can be timed around business performance and member demand rather than legislative timelines.

ELIGIBILITY

- Small business entities with aggregated annual turnover under $10 million

- Assets must cost less than $20,000 per item (GST-exclusive for GST-registered businesses)

- Assets must be first used, or installed ready for use, from 1 July 2026 onwards

2. Two-year loss carry-back

EFFECTIVE 2026–27 | COMPANIES WITH TURNOVER UP TO $1B

WHAT IT IS

Under the two-year loss carry-back measure, incorporated businesses that make a tax loss can apply that loss against company tax paid in previous profitable years and receive a refund of tax already paid. The refund amount is capped by the company’s franking account balance.

Originally introduced during the COVID period as a temporary measure, the policy has now been permanently reintroduced and expanded to businesses with turnover up to $1 billion. Treasury estimates approximately 85,000 Australian companies will benefit.

WHY IT MATTERS FOR FITNESS AND WELLNESS OPERATORS

For multi-site operators, franchise groups and growing businesses operating under a Pty Ltd structure, this creates real flexibility during high-investment periods.

Expansion years are often the most cash-intensive stages of growth. Opening a new location, upgrading facilities, replacing equipment fleets or entering a new market can all temporarily drag down profitability, even when the long-term outlook is strong. The loss carry-back helps offset some of that pressure by letting businesses recover tax paid during stronger trading years, improving cash flow right when reinvestment costs are at their highest.

Worked example

A functional fitness business operating across two locations paid a total of $30,000 in company tax across the 2024–25 and 2025–26 financial years.

In 2026–27, the business opened a third location. Between fit-out costs, equipment purchases, staffing and pre-opening expenses, the expansion results in a $60,000 tax loss for the year.

Under the loss carry-back measure, the business may be able to recover up to $15,000 of company tax previously paid (based on the 25% company tax rate), subject to its franking account balance.

For operators in growth mode, that refund can make a meaningful difference during the exact period cash flow is under the most pressure, when investment costs are high, new locations are ramping up, and profitability is still stabilising.

PRACTICAL CONSIDERATIONS

- Only available to incorporated businesses, sole traders and partnerships are not eligible

- Applies to revenue losses only, not capital losses

- Refunds are capped by the company’s franking account balance

- Claimed through the company tax return for the relevant loss year

3. Loss refundability for new start-ups

EFFECTIVE 1 JULY 2028 | FIRST TWO YEARS OF OPERATION

WHAT IT IS

From the 2028–29 financial year, eligible start-up companies in their first two years of operation can receive a cash refund tied to tax losses incurred during those early stages. Unlike the loss carry-back measure, it doesn’t refund previously paid company tax, most new businesses haven’t generated taxable profits yet.

Instead, refunds are linked to payroll-related taxes already paid to the ATO, including PAYG withholding and FBT on employee wages. Treasury estimates around 25,000 early-stage companies will benefit each year.

WHY IT MATTERS FOR NEW STUDIO OPENINGS

The first year or two of a new gym or studio are usually the most financially demanding. Fit-out costs, equipment, staffing, marketing and member acquisition all stack up before the business reaches full profitability. This measure helps ease some of that early pressure by letting operators recover part of the payroll-related tax already paid while the business is still scaling.

It’s particularly relevant for operators building employee-based teams, since PAYG withholding forms the basis of the refund calculation. Businesses that rely primarily on contractor models will see less direct benefit.

WHO THIS HELPS MOST

A new studio that pays $40,000 in PAYG withholding on employee wages in year one and records a $50,000 tax loss may be eligible for a refund of up to $40,000 from the ATO.

The refund is capped by the amount of PAYG withholding actually paid, not the size of the overall loss.

4. Permanent $1,000 instant work-related tax deduction

EFFECTIVE 2026–27 | INDIVIDUAL TAXPAYERS

WHAT IT IS

From 2026–27, Australian taxpayers can claim an instant $1,000 deduction for work-related expenses without needing to keep receipts or track individual costs. Workers with higher eligible expenses can still choose to claim under the existing rules instead. Treasury expects around 6.2 million Australians to benefit, with a significant reduction in compliance and admin burden at tax time.

WHY IT MATTERS FOR THE FITNESS WORKFORCE

This isn’t a direct business tax measure, but it’s worth knowing about for anyone managing a team. Employed personal trainers, instructors, front-of-house staff and studio managers can all claim a simplified $1,000 deduction through their individual tax return without maintaining detailed records for smaller expenses.

For self-employed PTs and contractors already claiming significant business expenses, the benefit will often be smaller. But for many employees with lower annual claims, it removes a real admin headache.

For employers, it’s also a decent EOFY communication opportunity, letting staff know about the deduction through onboarding resources or internal comms is a simple, low-effort staff engagement win.

5. Venture capital incentive expansion

EFFECTIVE 1 JULY 2027

WHAT IT IS

The Budget expands eligibility thresholds for two Australian venture capital investment structures: Early-Stage Venture Capital Limited Partnerships (ESVCLP) and Venture Capital Limited Partnerships (VCLP). Both provide tax-advantaged treatment for VC investment into Australian growth businesses.

Under the updated rules, the ESVCLP asset cap moves from $50 million to $80 million, and the VCLP cap moves from $250 million to $480 million. The change reflects that many modern growth businesses now scale past the old thresholds much earlier than they used to.

WHY IT MATTERS FOR FITNESS AND WELLNESS

For independent gyms and single-site operators, the direct impact here is minimal. This measure is most relevant for fitness tech companies, wellness platforms and larger multi-location operators pursuing growth capital or national expansion.

Under the previous thresholds, some Australian VC funds faced limitations when investing into later-stage growth businesses, particularly as valuations in the technology and wellness space increased. Widening those thresholds gives more eligible Australian capital room to back scaling businesses while retaining the tax-advantaged treatment.

For operators exploring private investment, technology-led expansion or multi-market growth over the coming years, this may improve access to suitable capital.

6. PAYG instalment flexibility

EFFECTIVE 1 JULY 2027

WHAT IT IS

Two changes here. First, an opt-in monthly PAYG instalment model. Most businesses currently pay quarterly, which creates larger cash outflows at specific points in the year. Monthly payments let businesses spread tax obligations more evenly across the operating cycle.

Second, an expansion of the ATO’s dynamic instalments pilot, which uses connected accounting software to calculate PAYG installments based on more current business performance rather than relying on prior-year estimates.

WHY IT MATTERS

Revenue in fitness and wellness rarely moves in a straight line through the year. January surges, quieter winter periods, seasonal membership trends and expansion phases all create fluctuations that quarterly installments don’t always reflect well. Under the current system, those instalments can overestimate tax obligations during slower periods and restrict cash flow unnecessarily.

The dynamic instalments model has real potential for operators already running integrated cloud accounting, booking and billing systems. It’s not a headline reform, but more accurate, responsive tax payments have a compounding effect on cash flow predictability, especially for businesses balancing recurring revenue with ongoing reinvestment.

7. What didn’t change (and what to watch)

CAPITAL GAINS TAX AND NEGATIVE GEARING

Changes to CGT and negative gearing were announced for property investments acquired from 1 July 2027. This includes replacing the current 50% CGT discount with a CPI-indexed model, a 30% minimum tax on real capital gains, and limiting negative gearing to newly built properties.

These sit well outside the day-to-day operations of most gyms and studios. They may still be relevant for operators who personally own the property their business runs from, businesses structured through trusts holding property assets, or operators with external investment property portfolios. They don’t change the taxation treatment of ordinary business operations, operating profits or business equipment.

SMALL BUSINESS CGT CONCESSIONS

The Government has kept existing small business CGT concessions in place. The 15-year exemption, 50% active asset reduction, retirement exemptions and rollover relief provisions all remain intact. For operators planning a future business sale or succession strategy, this matters, some of the most valuable long-term tax planning concessions available to business owners are still there.

PAYROLL TAX

No federal payroll tax changes in this Budget. State-level payroll tax obligations remain as they were, and operators expanding across multiple states should keep monitoring thresholds and compliance requirements, particularly in NSW, Victoria and Queensland where the rules differ.

ENERGY BILL RELIEF

The small business energy rebate ended on 31 December 2025 and wasn’t renewed. For operators running energy-intensive facilities (recovery spaces, saunas, steam rooms, HVAC-heavy environments) energy costs are going to keep being a pressure point.

Practical actions for operators

The impact of these measures will vary depending on business structure and growth stage, but there are a few practical areas worth reviewing with your accountant, adviser or finance team over the coming financial years.

BEFORE 30 JUNE 2026

- Review planned equipment and infrastructure investments for 2026–27, particularly anything likely to fall under the $20,000 write-off threshold

- Check franking account balances if loss carry-back might come into play during future expansion or heavy investment periods

- Assess whether monthly PAYG instalments could improve cash flow predictability once the option is available from 1 July 2027

DURING 2026–27

- Align equipment purchases and reinvestment decisions with business performance and growth plans rather than EOFY timing pressure

- Share the $1,000 instant work-related deduction with employees as part of EOFY comms or staff engagement

- For operators considering new site launches, look at whether the future start-up loss refundability measure might influence timing or staffing strategy

LONGER-TERM CONSIDERATIONS

- Businesses pursuing investment or expansion capital may benefit from the broader VC eligibility thresholds from 1 July 2027

- Operators holding property assets outside the operating entity should model the future impact of CGT and negative gearing reforms ahead of implementation

- Businesses investing in internal technology or proprietary systems should assess potential R&D Tax Incentive eligibility as the rules evolve from 2028 onwards

__

Disclaimer: This content is for informational purposes only and is based on our analysis of the federal budget announcements. It does not constitute legal, financial, or tax advice. If you are seeking to understand or negotiate your legal or tax position, we recommend obtaining independent professional advice.

Neil Davis is the CFO of Hapana, where he leads finance, compliance, tax, financial reporting, and capital strategy. With more than 20 years of executive experience across SaaS, fintech, and financial services, including multiple CFO roles and M&A transactions, he brings a strategic and operational perspective to supporting high-growth businesses as they scale. Neil is CA(SA) and CFA qualified, with deep expertise across financial strategy, governance, and growth-stage operations.

Get started with Hapana

- Manage members with ease

- Migrate your data hassle-free

- Priority support from our team